Another Brick in the (Blend) Wall: Key thresholds and barriers for biofuels

We hear so much about the ethanol blend wall, that we can be excused for thinking it is the primary wall, or threshold, out there.

We hear so much about the ethanol blend wall, that we can be excused for thinking it is the primary wall, or threshold, out there.

The Growth Energy publicity juggernaut ceaselessly reminds us that, at 10 percent blends of ethanol, the US can absorb only about 13 billion gallons of ethanol before it has nowhere to market its ethanol fuel, given the tepid distribution options for E85.

But even were the US EPA to approve E15 ethanol blending, there are some other significant walls and thresholds to keep in mind.

Here are the Digest’s Top 10.

1. The $60 oil parity wall.

At the 2010 Advanced Biofuels Leadership Conference, Coskata CMO Wes Bolsen said, “If we didn’t believe that the price of oil was ultimately going to reach $100, none of us would be here.” We haven’t yet seen that $100 oil is a sustainable price for the world’s most important energy carrier – the $135 levels seen in 2008 plunged the globe into a wrenching recession. But most advanced biofuels companies are modeled on parity with far lower oil costs. Their goals: Parity, at scale, with $20-$80 oil. Factors such as the value of co-products and rosy assumptions on yields at scale may be a reason to discount some of the more aggressive assumptions on parity. Threshold: at scale, advanced biofuels will generally be competitive with $60 per gallon oil, which translates into $1.50-$1.60 wholesale fossil fuel. Right now, cellulosic ethanol using enzymatic hydrolysis is aiming at the $2 per gallon mark, with enzyme costs continuing to fall and process yields rising.

2. The 23 gram algae viability wall.

23 grams per square meter per day. Sustainably above that yield, algal biofuels can be a goldmine. With a 25 percent oil content and 8 percent carbohydrates (available for fuel conversion), algal fuel systems can yield around 3000 gallons per acre. Below those yields, open ponds start to have challenging economics. That’s one of the reasons why PetroAlgae opted to commercialize their lemna platform first, where they have realized 40 grams per square meter per day in their one-hectare demonstration system.

3. The 19.5 billion gallon blend wall for E15.

After the E10 blend wall, cometh the E15 blend wall, clocking in at 19.5 billion gallons. The 2015 US target for 2015, under the Renewable Fuel Standard, would bring us right there, and by 2016 we’ll have the blend wall all over again. Drivers, start your (lobbying) engines!

4. The 40 billion gallon blend wall for Bu19 biobutanol.

Well, biobutanol gives us some options, doesn’t it. As we have reported in the Digest, biobutanol is generally approved for blending today at 60 percent higher levels than ethanol. Companies like Butamax and Gevo can generate about 80 Mgy of biobutanol from a 100 Mgy nameplate corn ethanol plant. Those gallons get a 1.3 per gallon RIN credit from the EPA. Putting those two metrics together, the US could meet its 36 billion gallon 2022 target with 27.7 billion gallons of biobutanol RINs, and 140 billion gallons of gasoline demand can tolerate up to 26.6 billion gallons of biobutanol if E12 is approved, which would generate 34.6 billion RINs. The rest could easily come from the diesel side.

Yep, that means no ethanol pipelines, no need for E15, no blender pumps, and using existing corn ethanol infrastructure. That’s one reason we are bullish at the Digest on the prospects for biobutanol.

5. The 2.5:1 EROEI wall. That’s energy return on energy invested, for the blissfully uninitiated. The EROEI os sugarcane is 7 to 1 – that is you get 7 units of energy for every unit of energy you put into conversion. That’s popular. In days of yore, corn EROEI was measured at anywhere from 1 to 1 to 1.3 to 1. That’s unpopular. The returns have increased from corn to 2 to 1, and there’s still a lot of muttering. So we put this threshold at around 2.5 to 1, where the debate drifts away and people look at the benefits of the fuel.

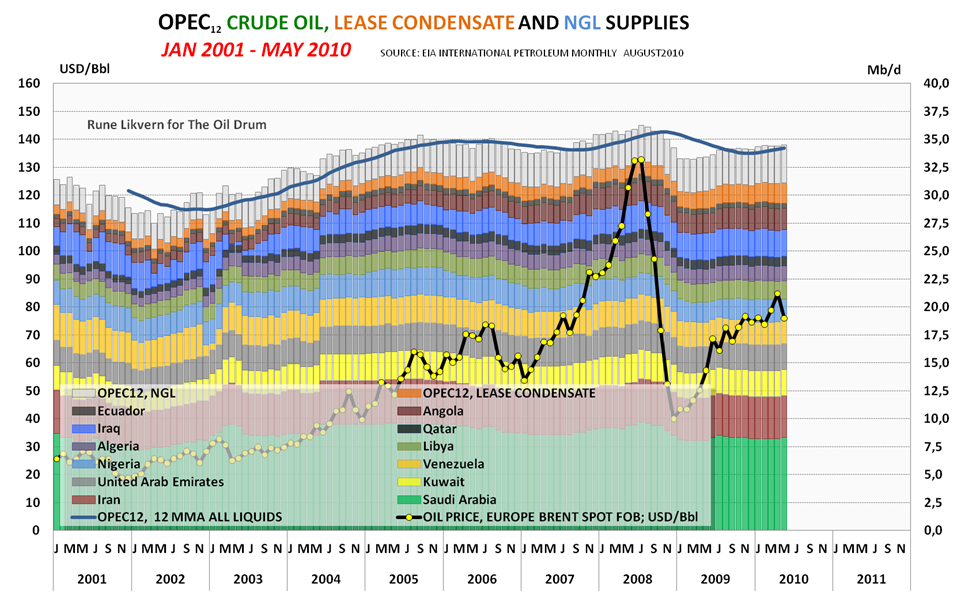

6. The 536 billion gallon energy security wall .

How much wood can a woodchuck chuck? In the case of OPEC, they chuck 536 billion gallons of crude oil into the market every year, for fuels, chemicals, plastics and a myriad of co-products.

7. The 150 million acreage wall.

How much acreage is really available for biofuels development. This is the food versus fuel conundrum. There is little argument about the central tenet of indirect land use change theory: universally agreed, at some point there could be so much energy crop production that it would unsustainably distort the acreage for food production, possibly resulting in the conversion of carbon reserves (or precious habitat) such as the Amazonian rainforest. Like peak oil or global warming, the question is really not whether, but when. Critics say that ILUC is happening now, others say there is no data to support such a conclusion.

What’s real? Today, there are around 7 billion arable acres. To replace just the OPEC exports of oil (i.e. global energy security), would require 1 billion acres of corn, 768 million acres of sugarcane, 267 million acres of poplar, or 177 million acres of algae. Since poplar grows in poorer soils, and algae grows in completely non-productive areas, those are easier bets. The sugarcane and corn acres are very tough to envision just on the limitations in the geography in which they can be successfully cultivated at current or better yields. The US uses around 28 million acres of corn starch production, not affecting the protein stream, for ethanol, and look at all the squawking. Past 100 million global acres of arable land available for crop cultivation, the noise from all the protests would make the acreage unsustainable, regardless of the economics or the science.

8. The 560 million tonne animal feed wall.

Virtually all (but not all) biofuels and advanced biofuels processes create a leftover biomass, which generally is marked for distribution as animal feed. Because protein content and omega-3 levels can be high, some ventures have extravagant expectations of feed prices in the $1000 per tonne range. But how much extra biomass can animals eat?

The FAO tells us that animal feed demand is expected to reach 1.4 billion tonnes by 2020. Now, animals eat a mix of foods, never more than around 40 percent any one source by weight. That leaves us with about 560 million tonnes of potential replacement. Given that there is generally (but not always) two tons of feed for every ton of fuel, that means we have around 280 million tons of fuel that can be produced before the feed markets can’t absorb the biomass — with power gen the next best option, at far lower prices, which messes with the economics. That’s about 76 billion gallons of fuel. After that, the economics start to get dodgy – and microbial fuel conversion systems like we see Amyris, LS9 and Joule.

9. The 1 ton per acre biomass residue wall.

In Iowa, POET is offering guidance to farmers that they can sustainably remove up to 1 ton of biomass residues per acre for cellulosic ethanol production, without altering their fertilizer or other land-management strategies. At rates of $60 per ton, that biomass is worth an additional $60 per acre for a corn farmer, adding 10 percent to farm revenues based on current corn yields and prices. That’s a material boost for farmers, who also could benefit in the near-term from USDA incentives of up to $40 per ton, which would add even more incentive for the farmers.

If those numbers prove correct, there is around 85 million tons of feedstock available today just from the US corn harvest, enough to sustainably produce 6.8-8.5 billion gallons of cellulosic ethanol, while adding up to $5 billion to US corn farmer income before accounting for USDA transitional subsidy payments.

Researchers point to similar tonnage available from wheat and soy cultivation, indicating that there is something on the order of 200 million tons of biomass , enough to produce 16 million gallons of cellulosic ethanol and add $12 billon to farm income.

The key metrics? The tonnage of biomass that can be sustainably removed, and the price per ton of biomass. They are slippery. In states with Renewable Power Standards, where biomass is often the most reliable, affordable short-term source of renewable power, prices can soar to $110 or more per ton of biomass. That makes biomass generally unfeasible for fuel conversion. And researchers do not yet precisely agree on the tonnage of biomass that can safely be removed. If that figure could be safely doubled through innovations in plant genetics or farm practices that reduce fertilizer needs, the yields go up correspondingly.

10. The aforementioned 13 billion gallons US E10 blend wall.

Category: Top Stories

{kind=link}