You Can’t Fly with Lead Wings, or Corn Ethanol’s SAF CI Problem

By Steven Slome, Jia Ming Ong and Matthew Morton

Special to The Digest

For a more in depth discussion, please see our recent whitepaper.

The View from 10,000 ft

Over the last decade, aviation transport’s growing contribution to anthropogenic climate change has been acknowledged by both the industry and major governments, and ambitious goals have been put in place to cap and then reduce its GHG net emissions to zero by 2050. Unlike road and marine transport, decarbonization of aviation via alternative propulsion options such as electrification or hydrogen is currently highly challenging, particularly for the large, long-range aircraft that account for a significant proportion of the important air passenger and freight transit markets. Accordingly, the main tool for achieving the goal of aviation decarbonization is currently liquid Sustainable Aviation Fuel (SAF). SAF production is poised to grow significantly, supported by governmental measures such as consumption mandates (in the EU) and generous tax credits (in the United States).

At present, SAF production is dominated by lipid feedstock-using Hydrotreated Esters and Fatty Acids (HEFA, also known as HVO) processes, which are technically proven and increasingly commercialized. However, growth of this technology to the scale required to decarbonize global aviation is blocked by a range of barriers, not least by likely constraints on the availability of sufficient low Carbon Intensity biomass feedstocks.[1] Based on current projections of feedstock availability and rate of technological progress, global SAF production by 2050 will fall well short of targets. By 2050, NexantECA sees SAF contributing between 15 and 20 percent of total jet fuel demand[2], significantly short of targets set by governments and industry bodies, many of whom are targeting at least 60-80 percent of SAF use to support their respective net zero goals. If this proportion is to increase significantly, emerging routes to SAF will need to scale up considerably and rapidly.

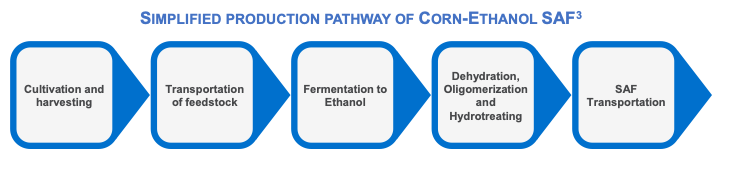

Among the most promising emerging routes is Alcohol-to-Jet (ATJ) production, which uses bioethanol – already widely in use as a biomass-derived gasoline blendstock – as its primary feedstock. ATJ production entails the dehydration of ethanol to ethylene, followed by oligomerization and subsequent hydrotreating to produce SAF or other drop-in fuel products, as shown in the Figure below:

ATJ SAF is being viewed as a likely long term SAF option most particularly in the United States, the world’s major producer of ethanol, largely from corn feedstock[4]. As long-term ethanol demand falters due to an effective 10 percent ceiling on blending into gasoline (the “blend wall”) in most markets, and the likely erosion of overall gasoline use by road vehicle electrification, US corn ethanol is likely to be more widely available, reducing constraints on SAF feedstock availability. It is also politically beneficial in the US to expand (or at least maintain) the market, as corn ethanol is a major product of the US Midwest.

Two key barriers stand in the way of greater corn ethanol use in SAF production (assuming continuing technological progress on production scale-up), both of which are linked to the regulatory drivers of biofuels consumption. Firstly, as a food/animal feed crop, corn – and most other feedstocks for large scale ethanol production such as sugarcane and wheat – are effectively barred from contributing to SAF consumption targets in the European Union, which is likely to be one of the world’s major SAF markets. EU policy support for SAF is strong, most notably through the clear mandates on SAF consumption through to 2050 represented by the RefuelEU Aviation regulation finalized in 2023, which demands a 70 percent share of total jet fuel by 2050 (of which 35 percent is intended to come from e-fuels). However, as with previous EU biofuels policy – notably successive iterations of the bloc’s Renewable Energy Directive dating back to 2012 – a clear priority is the avoidance of competition with food production, and a concern over the life-cycle Carbon Intensity of biofuels from food crops, including the impacts of Indirect Land Use Change (ILUC). Accordingly, the RefuelEU Aviation mandates explicitly bar food or feed crop use in SAF production from counting towards mandates. Unless advanced (cellulosic) ethanol production can scale up very significantly, there is therefore little scope for ATJ SAF use to take off in Europe.

No such regulatory barriers on food competition exist for SAF in the United States or in many other markets. However, regulatory requirements are also linked to the second main barrier to increased corn ethanol use in SAF, which is the fact that it has a relatively lower ability to reduce aviation emissions – and therefore to qualify for government support – than some other SAF feedstocks.

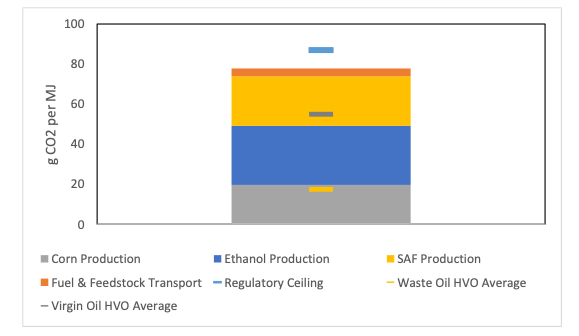

As noted, U.S. support mechanisms for SAF and other biofuels are increasingly based on incentivizing fuels with the lowest Carbon Intensity possible. California’s state-level Low Carbon Fuel Standard allows producers to earn credits depending on the CI improvement of their output compared to petroleum-based fuels, while the Inflation Reduction Act awards a US$1.25-1.75 per gallon Blenders Tax Credit to producers meeting set CI criteria. The CI of corn ethanol-based SAF is on average around 50g CO2e/MJ. The regulatory standard (e.g. in the California LCFS) is set at around 87 g CO2e/MJ in 2024, and is targeted to decline further to around 80 g CO2/MJ by 2030[5]. This may not seem to put corn ethanol SAF at a disadvantage, but once processing emissions, indirect land use change (ILUC), feedstock and product delivery are included, the CI of ATJ SAF is just about at the ceiling. The CI of SAF production can vary based upon configuration, however average estimates range from around 20 g CO2/MJ, resulting in a finished CI of over 70 g CO2/MJ. The Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA), a market-based measure introduced by the International Civil Aviation Organization (ICAO), estimates the lifecycle emission of corn ethanol-based SAF at around 66 g CO2/MJ in the US, reaching around 91 g CO2/MJ after taking into account indirect land use change (ILUC).[6] Furthermore, for the resultant SAF to qualify for the US$ 1.25 per gallon Blender’s Tax Credit (BTC) offered under the Inflation Reduction Act, the SAF product must be certified to achieve a minimum lifecycle greenhouse gas emissions reduction percentage of at least 50 percent, something of a challenge if corn ethanol based SAF is produced based on current processes without substantial improvements.

Carbon Intensity Breakdown Of Average Ethanol-Based SAF[7]

In contrast, waste oil based feedstocks (e.g., used cooking oil or tallow) used in HVO production can result in finished fuels with significantly lower CI, frequently in the range of 15-20 gCO2e/MJ, while virgin oils such as soy oil can be as high as 55 gCO2e/MJ but still well below the level of ethanol-based production. In order to be able to benefit from full regulatory support (thus expanding ethanol’s available market), the production of corn, ethanol and SAF will need to find a way to reduce their respective footprints, as these are the largest contributors to ethanol SAF’s lackluster CI. Fuel and feedstock transport is the smallest contributor. As shown in the graphic, ethanol production is the largest contributor to the CI of the produced SAF, followed by the SAF production process, and finally the corn production itself. In order to compete against waste oils, dramatic reductions are required—although modest reductions are required to compete with virgin oils. Though it should be noted that if net zero production is sought, even larger and more bold reductions are required.

As of early 2024, the eventual ability of corn ethanol-based SAF to benefit from US government support mechanisms remains the subject of ongoing discussion. Principally, the government has come under pressure from, on the one hand, ethanol and corn producers, and on the other hand, several environmental groupings, over which form of Carbon Intensity modelling should be used to define the CI of ethanol SAF. The standard model (the Greenhouse Gases, Regulated Emissions and Energy Use in Technologies, or GREET model used by the Department of Energy) tends to enable ethanol SAF to meet required CI levels, while environmental groups have argued for more stringent modelling and the prioritization of waste-based feedstocks. In late December 2023, the US government reportedly signaled a compromise whereby the GREET model would remain in use, but may be modified in the near future.

Better SAF than Sorry: Advantages of Corn Ethanol as a SAF feedstock

With such a high CI from the start, one might rightly wonder why corn ethanol is worth the trouble as a feedstock. There are several key advantages that ethanol has over other SAF feedstocks that cannot be ignored.

Feedstock Supply

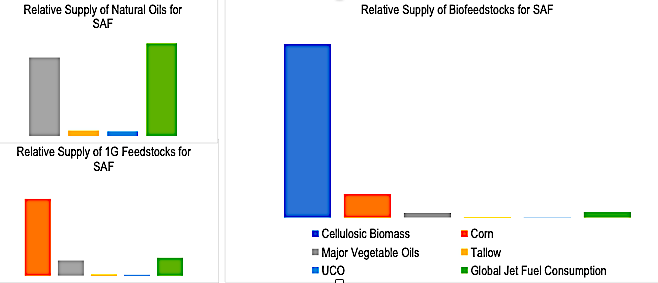

As stated previously, feedstock availability is a major concern—but most don’t realize the scale of the differences. Low CI oil feedstocks such as tallow and UCO make up only a small percentage of oils supply (around 10 percent), while the rest is supplied by higher CI virgin oils (over a third of which is palm with notable broad sustainability issues). Additionally, this supply of oils has many existing end-uses to supply including food, oleochemical, and personal care which also require significant volumes. Corn supply is roughly 4.5 times total oil supply—and while corn also has many existing end-use markets (including food and animal feed), the supply excess of corn is so great that unlike natural oils it actually is larger than global jet fuel consumption currently. Corn ethanol as a feedstock also opens the door to cellulosic ethanol. While cellulosic ethanol has had notable difficulties in commercialization, the allure of lower CI ethanol and great increases in available biofeedstock supply have continued the interest.

Supply of Biofeedstocks For SAF[8]

Getting Past the Blendwall

Most routes are stuck behind a 50 percent blendwall—meaning their product cannot be used neat, and instead must be blended with a fossil fuel at least 50 percent. This is not optimal for many reasons. Additionally, several test flights (including notably Virgin Atlantic Airways) have occurred on neat mixtures of sustainable isoparaffin and aromatics, with the intent of proof of concept for getting past this blendwall. Ethanol is among the two approved routes currently for mixtures containing aromatics (Annex A4 and Annex A8), as well as having potential integration opportunities with aromatics production (e.g., Ethanol to Aromatics and/or the Vertimass CADO technology).

Integration Potential

Corn ethanol offers potential integration opportunities not necessarily available to other SAF feedstocks and processes:

- Carbon Capture Ready: Fermentation to ethanol produces a concentrated stream of CO2 that can be captured. Many other routes (e.g, HVO) do not have a readily available substantial stream of biogenic CO2that can be captured easily. A roughly equal amount of CO2 and ethanol is produced.

- Potential for Integration with Aromatics: As stated previously, one approach to getting past the SAF blendwall is to use aromatics. Development of the ethanol to aromatics (and ethanol to gasoline) technology allows for potential integration opportunities and synergies in production of a finished SAF that doesn’t require blending with a fossil fuel. Few other routes still under development are being pursued with this type of integration.

Getting the Lead Out: Shrinking the Carbon Footprint of SAF

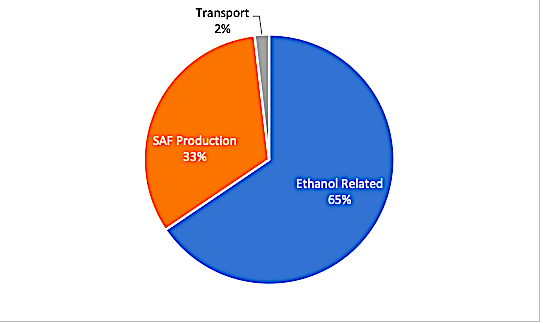

SAF production from ethanol can be carbon intensive—though most of the emissions are related to the corn and ethanol production itself (almost two-thirds). Several approaches are being undertaken to reduce the CI of SAF production. Though considerably smaller than the combined ethanol and corn contributions, reductions here are also important, as some corn-based and ethanol-based emissions will be hard to mitigate.

Carbon Intensity of Corn Ethanol-Based SAF[9]

Approaches aimed at emissions across the value chain include:

- Fertilizer decarbonization

- Regenerative agriculture / alternative agricultural practices

- Electrification with renewable power

- Advanced ethanol / alternative feedstocks

- BECCS

- Biogas integration

- Catalyst advances

- Blue/green hydrogen

Announced Plans: Low CI Alcohol-Based SAF on the Radar

A few developers have currently planned low CI ethanol-based (and other alcohol-based) SAF. Listed subsequently are the current developers making notable efforts with planned commercial production of SAF and associated products in the next few years:

- Gevo: Net-Zero 1 Project for 65 million gallons per year of products

- LanzaJet: LanzaJet Freedom Pines Fuels for 10 million gallons per year of products

- Vertimass: Vertimass / Ekobenz sustainable fuel plant for eight million gallons per year of product

- Swedish Biofuels: Swedish Biofuels for approximately 90 thousand tons per year

Key NexantECA Insights Reports on the Subject

NexantECA consultants have additionally been very active in evaluating technoeconomic, carbon intensity, and market developments in the sustainable fuels and chemicals space, particularly as it pertains to corn, ethanol, and SAF value chains. In addition to significant bespoke consulting work in this area, NexantECA has also published the following related reports that may be of interest to readers:

[1] Source: NexantECA’s Market Scenario Planning: Renewable Feedstock Availability to 2050 (2023)

[2] Source: NexantECA’s Market Insight: Sustainable Aviation Fuel (SAF) (2023)

[3] Source: NexantECA’s Biorenewable Insights: Ethanol to Jet (2024)

[4] While minor byproducts from corn processing (e.g. technical corn oil (TCO) or distiller’s corn oil (DCO) can also be hydroprocessed to derive low CI SAF, this discussion specifically refers to the use of corn grain, converted to ethanol via fermentation and subsequently SAF via the ATJ pathway.

[5] Source: CAARB, https://ww2.arb.ca.gov/sites/default/files/2020-09/basics-notes.pdf

[6] Source: ICAO document – CORSIA Default Life Cycle Emissions Values For CORSIA Eligible Fuels https://www.icao.int/environmental-protection/CORSIA/Documents/CORSIA_Eligible_Fuels/ICAO%20document%2006%20-%20Default%20Life%20Cycle%20Emissions%20-%20June%202022.pdf

[7] Source: Argonne GREET, NexantECA Analysis

[8] Source: NexantECA’s Market Scenario Planning: Renewable Feedstock Availability to 2050 (2023)

[9] Source: Argonne GREET, NexantECA Analysis

Category: SAF, Top Stories