Renewable Diesel (HEFA) Plant Conversions for Maximum SAF Production

By: Mark Robertson

Special to The Digest

Renewable diesel (“RD”) and sustainable aviation fuel (“SAF”) can be produced by hydrotreating virtually any type of biogenic feedstock lipid (oil). In processes involving hydrotreated esters and fatty acids (“HEFA” processes), the most common feedstocks are animal fats, waste greases, and vegetable oils, which are made up mostly of triglycerides. HEFA facilities can be configured to maximize RD or SAF production.

Over time, HEFA RD production facilities may transition to maximize SAF production due to the migration of light-duty, medium-duty, and bus fleets from diesel to electrification, growing SAF demand driven largely by government incentives, policy and mandates, as well as airline SAF commitments. HEFA facilities producing RD can redirect their focus to the SAF market, given the absence of a viable alternative technology solution (e.g. electrification or hydrogen combustion) for commercial aviation in the near or medium term.

RD Plant Description

Note that bio-based feedstock oils can be co-processed with petroleum-derived feedstocks in oil refinery units at relatively low coprocessing biogenic fractions, however, the following discussion focuses on standalone HEFA RD processing units.

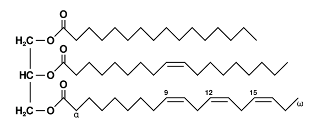

Figure 1: Typical triglyceride[1]

Triglycerides are composed of a three-carbon glycerol backbone and three fatty acid chains, with fatty acid carbon chain lengths typically from 12 to 22 carbon atoms. Hydrotreating of the triglycerides via (hydro-) deoxygenation (“HDO”) and decarboxylation reactions consume hydrogen, generates liquid petroleum gas (“LPG”), carbon oxides, and water, breaks the bonds between the glycerol backbone and the fatty acids, and saturates double bonds in the fatty acids, resulting in the production of saturated normal paraffinic hydrocarbon chains with carbon lengths from 11 to 22 carbon atoms (i.e. C11 to C22). Note that jet fuel typically has hydrocarbon molecules in the C5-C16 range and diesel fuel is typically C8-C24, so HEFA processes can produce both jet and diesel range fuel products, and the yield of both products depends on the feedstock composition.

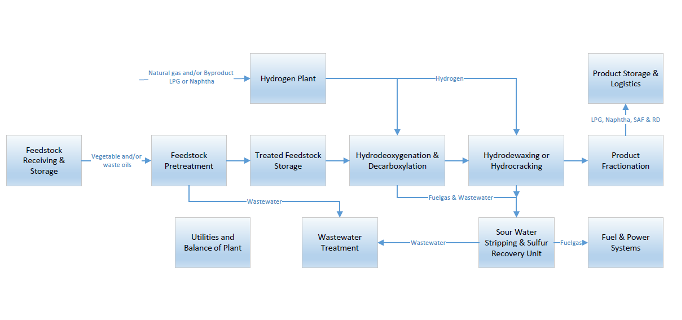

Figure 2: Renewable Diesel Plant

Feedstock vegetable and/or waste oils are received and offloaded at unloading racks from tank trucks, rail cars, or barges and are pumped to (heated) storage tanks. The feedstocks may be blended from the feedstock storage tanks before being pumped to the pretreatment unit. At the pretreatment unit, the feedstock oil is degummed and dried. Additional pretreatment steps may include chloride removal, polyethylene removal, clay adsorption, or bleaching. The pretreated feedstock will typically be stored in tankage before downstream processing.

Pretreated feedstocks are pumped to the Renewable Diesel Unit (“RDU”). In the RDU the feedstock oils are reacted with hydrogen in the presence of multiple catalysts in fixed bed reactor(s) at high pressure and temperature. The reaction products are cooled, and liquid (condensed) products are collected in a high-pressure separator prior to the uncondensed vapor being either returned to the reactor(s) loop or purged from the high-pressure separator. Hydrogen is provided to the reactor loop at a make-up rate which maintains the desired hydrogen partial pressure in the reactor(s). Condensed liquids from the high-pressure separator are let down to low pressure. These low-pressure liquids are pumped to a fractionation unit, which uses fractional distillation to make the necessary product cuts, to meet the required product specifications, including for the renewable diesel. Finished fuel products and byproducts are pumped to downstream storage, blending, and loading systems. Other required process units include a hydrogen plant, wastewater treatment unit, sour water stripper, and sulfur removal unit as well as all the necessary utility and outside battery limits (“OSBL”) systems.

RD and SAF Production

Although normal paraffins are ideal for high diesel fuel cetane, they result in poor cold flow properties (cloud pt and cold filter plugging pt in the case of renewable diesel), whereas iso-paraffins result in significantly improved cold flow properties. Hence, it is necessary to isomerize a portion of the product oil, after HDO reactions, to ensure that the resultant renewable diesel meets the cloud point specification. These hydroisomerization reactions produce iso-paraffinic compounds in the product oil, with better cold flow properties than the normal paraffins, and are typically labeled as hydrodewaxing reactions (“HDW”). HDW reactors also result in some limited cracking of larger hydrocarbons into smaller chain molecules, so some fuel gas, LPG, and naphtha are produced in the HDW reaction step. Note also that the carbon number of the product oil cannot exceed the typical maximum for diesel fuel specifications (approx. C24), so it is not required or particularly desirable to crack any of the product oil to smaller carbon chain lengths, if obtaining a maximum renewable diesel yield in the product oil is desirable.

If maximum jet fuel range products are desired it will still be necessary to first complete the HDO reactions of the feed oil, before proceeding to hydrodewax the jet fuel to meet cold flow property requirements (freeze point) and hydrocrack the product oil to maximize the yield of hydrocarbon molecules in the jet fuel range (<C16). Hydrocracking (“HDC”) purposely cracks the longer chain hydrocarbons into smaller shorter chain hydrocarbons, resulting in some RD and SAF yield loss to fuel gas, LPG, and naphtha, in addition to other reactions including isomerization and some limited cyclization and aromatization reactions at more severe hydrocracking reaction conditions. Hydrocracking reactor conditions are more severe than other HDO and HDW reactions and require a different catalyst. The severity of the hydrocracking reaction can be varied to adjust the extent of cracking and the resultant jet and diesel yields, so HEFA plants with hydrocracking reactor(s) can have a high degree of product flexibility.

HEFA plants focused on maximizing RD production typically omit the more expensive HDC reactors and catalysts, experiencing less yield loss to fuel gas, LPG, and naphtha, and consuming less hydrogen. However, they must still include the fundamental process steps of HDO and HDW reactions. With appropriate fractionation equipment, these plants can still extract a portion of the liquid fuel produced as a lighter SAF cut (typically < 20 vol%).

HEFA plants designed for increased SAF yield are equipped with hydrocracking (HDC) reactors and catalysts. The HEFA plant’s ability to switch between jet fuel and diesel production depends on factors like allowable reaction severity in the HDC step, catalyst loading and types, acceptable fuel yield loss, hydrogen availability, and downstream fractionation equipment design. While it is feasible to design for 100% SAF production, most plants are configured for a mix of jet and diesel production (typically < 80% SAF).

RD Plant Conversion Scope

Relatively minor operational and equipment modifications can allow HEFA plants originally configured or designed for maximum RD production to marginally increase SAF yields, but these plants typically require more significant retrofits to maximize SAF production. The scope of these necessary modifications will depend on the original plant design but can include the addition of hydrocracking/hydroisomerization reactors and/or catalysts, compression modifications to address additional reactor loop pressure drop, feedstock receiving and storage modifications and/or additions to fractionation equipment, additional product (SAF) and byproduct (LPG and naphtha) storage, blending and logistics systems, expanded hydrogen generation equipment and associated utility and OSBL system modifications.

As well as any necessary equipment changes required to be able to operate a HEFA facility in a max SAF mode, it is also necessary to address the increased plant production flexibility, in particular the ability to change the production mix of RD and SAF and variable LPG, naphtha and fuel gas production and hydrogen demand. This flexibility will impact equipment design but will also require the plant control systems to be designed to allow for this increased flexibility of operation.

Increased naphtha and LPG production may be partly utilized to generate the additional hydrogen required for max SAF production, via steam reforming of one or both of these feedstocks, but if product offtakes for this additional byproduct are not available or commercially attractive, these (renewable) fuels, plus the additional available fuel gas, could also be utilized on-site for steam and/or power generation.

Feedstock pretreatment requirements should be carefully reviewed with the HDC catalyst supplier to assess if there are any necessary pretreatment system design changes and if this would result in any impacts on the wastewater treatment plant operation.

Materials of construction in the hydrotreating unit(s) should be reviewed carefully, particularly given the more severe HDC reactor(s) operating conditions.

RD and SAF Economics

The current SAF value stack, SAF targets and mandates, and increasing SAF demand are incentivizing current and planned HEFA RD production facilities to consider conversion of the facility to maximize SAF production, at the expense of RD production.

The US is aiming for a 100% replacement of conventional aviation fuel (CAF) with SAF by 2050[2]. The EU’s SAF mandate increases from 6% in 2030 to 70% by 2050[3]. Other countries are developing SAF policies. In addition, many airline industry SAF commitments are equally or more ambitious than the US and EU targets. SAF produced through the HEFA pathway is expected to make up the vast majority of the US SAF production by 2030[4]. In the EU however, feed-crop derived vegetable oils are ineligible for SAF production, so HEFA SAF production may be more constrained by non-food/feed crop oil supply.

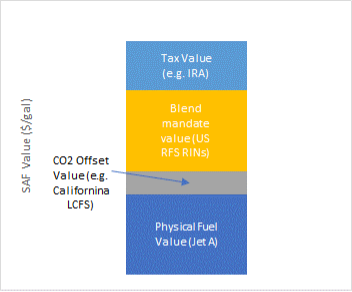

In the US, the SAF value stack includes the physical fuel value (Jet A-1), Renewable Fuel Standard (“RFS”) RIN value, California (or other state) LCFS credits, and Inflation Reduction Act (“IRA”) Blenders Tax Credits (“BTC”) or Clean Fuel Production Credits (“CFPC”). The primary drivers for the conversion of RD plants to maximum SAF production are currently the IRA credits and other state tax credits for SAF[5][6]. RD plant owners are closely monitoring the relative value stacks for SAF and RD and in several cases are planning for RD Plant conversions or new plant designs to maximize SAF production[7][8][9].

Figure 3: SAF Value Stack

The economics of an RD Plant conversion for maximum SAF production will greatly depend on the capital cost of the project, which is directly related to the required project scope. When RD Plant owners or project developers believe that the incremental revenue generated by the SAF and RD value difference exceeds the costs associated with RD Plant conversions, they will seriously consider converting their RD Plant to maximize SAF production.

For example, if a 100 MMGPY RD Plant requires US$120MM to convert the plant to maximum SAF production, the plant owner may require a differential in the value stack between SAF and RD of approximately $1.75/gal to justify the conversion project, obviously dependent on a large number of project-specific conditions.

The current difference in the SAF and RD value stacks wouldn’t warrant the conversion of the example facility (i.e. it is less than $1.75/gal), even with the IRA SAF provisions, but additional SAF policy support such as new state tax credits, airline industry ambition as well as SAF mandate penalties are contributing to continued interest in HEFA RD plant conversions and new HEFA SAF Plant planning and construction.

Conclusions

Owners of operating RD Plants and HEFA plant project developers are monitoring closely the (current and forecast) RD and SAF value stacks, as well as other policy and airline industry developments. HEFA technology is readily able to be configured for maximum SAF production, but it remains to be seen if financial incentives can be aligned to overcome project costs and enable HEFA RD Plant conversions to maximum SAF production, to contribute significantly to planned SAF production in the short to medium term.

About the Author

Mark Robertson has a Bachelor of Engineering (Chemical) with honors from Sydney University, is a registered Professional Engineer (PE) in the State of Colorado. He has over 30 years of experience in technology development, plant operations, and engineering, and has been involved in the conceptual design, engineering, construction, and operation of biofuels plants producing biodiesel, bio jet, methanol, and ethanol as well as several waste-to-energy and biomass-to-energy projects. Most recently he has completed techno-economic assessments on high-pressure biomass gasification, biomass refueling, renewable natural gas, biomass power, and ethane to aromatics technologies and has conducted due diligence on multiple small-scale gas-to-liquids technologies. He has special technical knowledge in the areas of biomass gasification, synthesis gas technologies, gas conditioning and cleanup, biofuel and chemical synthesis, Fischer-Tropsch fuel synthesis, fluidization, and process design.

He serves as an expert with Lee Enterprises Consulting, handling matters involving gasification, pyrolysis, biofuel & biochemical synthesis, gas-to-liquids, biomass and waste-to-energy, Fischer Tropsch fuels, syngas, hydrogen, and fluidization.

About Lee Enterprises Consulting

Lee Enterprises Consulting has over 180 experts that can help navigate your bioeconomy needs. If you need assistance with your Bioenergy project(s), please contact us.

[1] https://www.triglycerideforum.org/triglycerides-triglyceride-rich-lipoproteins-and-remnants/

[2] “Memorandum of Understanding: Sustainable Aviation Fuel Grand Challenge.” Sept. 8, 2021. https://www.energy.gov/sites/default/files/2021-09/S1-Signed-SAF-MOU-9-08-21_0.pdf

[3] “70% of jet fuels at EU airports will have to be green by 2050” Sept. 13, 2023, EU Parliament press release.

[4] “SAF Grand Challenge Roadmap”, DOE, Sept. 2022

[5] Illinois Sustainable Aviation Fuel Tax Credit, https://www.bakerbotts.com/thought-leadership/publications/2023/february/illinois-sustainable-aviation-fuel-tax-credit

[6] Washington Senate Passes Bill To Establish SAF Tax Credits, https://biodieselmagazine.com/articles/washington-senate-passes-bill-to-establish-saf-tax-credits-2518575

[7] Diamond Green Diesel (DGD) Approves a Sustainable Aviation Fuel Project at Port Arthur, Texas:https://www.prnewswire.com/news-releases/diamond-green-diesel-dgd-approves-a-sustainable-aviation-fuel-project-at-port-arthur-texas-301735115.html

[8] Calumet’s Montana Renewables became the largest SAF producer in North America in Q2, https://www.greencarcongress.com/2023/07/20230728-calumet.html

[9] World Energy To Further Boost U.S. SAF Production, https://aviationweek.com/special-topics/sustainability/world-energy-further-boost-us-saf-production

Category: Top Stories